In December 2016, Mediapart and its partners in the journalistic consortium European Investigative Collaborations (EIC) revealed how Portuguese football star Cristiano Ronaldo had funnelled, over seven years, a total of 149.5 million euros in earnings from image rights and other commercial deals into offshore companies based in Panama, in the British Virgin Islands, Ireland and Switzerland.

The revelations prompted the opening last year in Spain, where the Real Madrid player resides, of an investigation into his alleged wilful evasion of 14.768 million euros in tax payments, which he has firmly denied. The investigation centres on a total four alleged tax fraud offences by the 33-year-old Portugal international player which prosecutors say he committed in a "voluntary and conscious breach of his fiscal obligations” between 2011 and 2014.

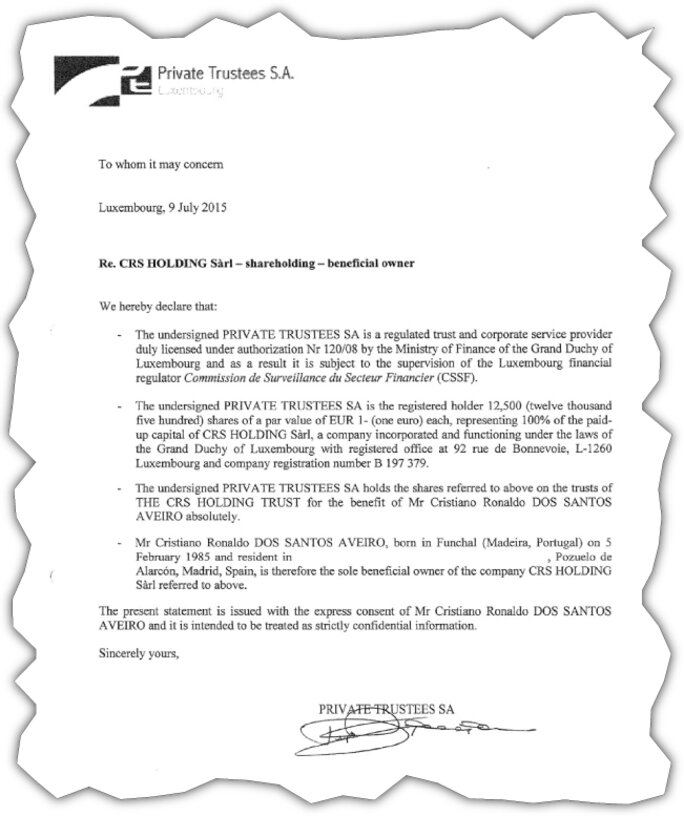

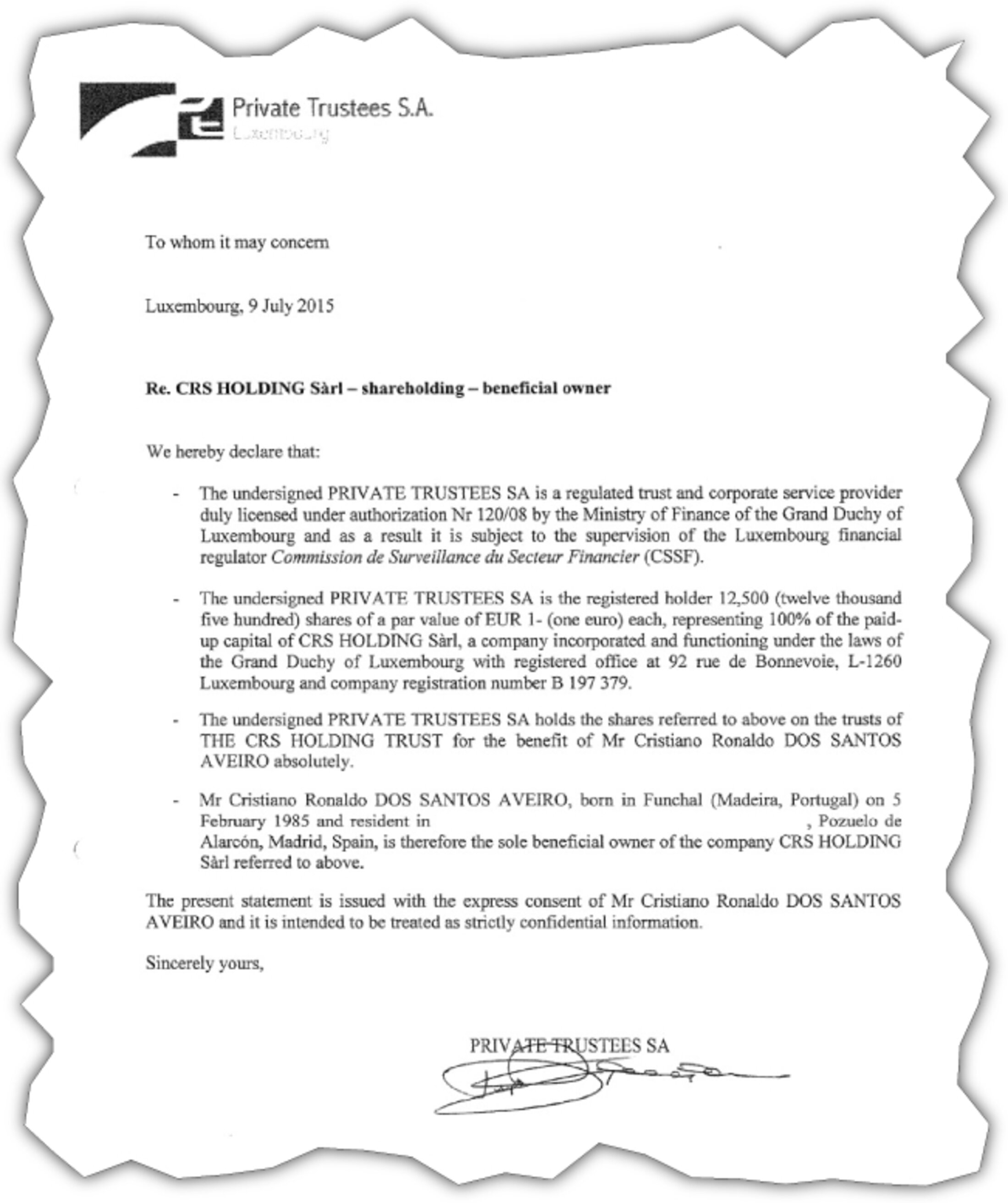

Enlargement : Illustration 1

After a series of court hearings before Spanish magistrates that continued into this month, a decision is imminent as to whether he should be sent for trial for the alleged fraud, when he would face a hefty fine and a potential 10-year prison sentence.

According to US magazine Forbes, Ronaldo is the highest-earning sports figure worldwide with a total income from his salary at Real Madrid and sponsorship deals during the 2016-2017 season estimated to total 83 million euros.

At one of the hearings in March, three fiscal experts called by Ronaldo’s lawyers to give their appraisal of the accusations against him surprised the court by agreeing with the prosecution case that he had committed tax fraud, even describing one of the defence arguments as the “most absurd” they had come across.

There is speculation that the footballer may reach a deal with prosecutors, but the Spanish media reported last month that an offer by his lawyers to the country’s tax authorities, the Agencia Estatal de Administración Tributaria, to pay a penalty of 3.8 million euros and provide an admission of wrongdoing in exchange for dropping criminal charges was rejected outright. According to Mediapart’s EIC partner El Mundo, Ronaldo is now prepared to offer 30 million euros in settlement of the case.

Enlargement : Illustration 2

Now, confidential documents obtained by German weekly Der Spiegel from the whistle-blowing platform Football Leaks and shared with Mediapart and other media partners in the EIC may further cloud the Madeira-born star’s situation. They reveal that in 2015, Ronaldo (whose full name is Cristiano Ronaldo dos Santos Aveiro) created a trust in the British Channel Island tax haven of Jersey, which in turn managed a Luxembourg-registered company to which it funnelled millions of euros. It appears that the activities of the Luxembourg company, whose registration documents make no mention of Ronaldo’s name, was centred on his commercial partnership with a Portuguese hotel chain.

While there is nothing illegal about his ownership of the trust in Jersey the documents obtained by the EIC also show that its existence was not mentioned in his tax returns in Spain for the year 2015.

Meanwhile, the EIC also understands that Ronaldo’s agent, Jorge Mendes, one of the most prominent agents in international sport, is the target of an investigation by tax inspectors from Britain, Cyprus, Ireland, the Netherlands, Portugal and Spain into his tax situation in 2015 and 2016. On the initiative of the Portuguese tax authorities, tax administration officials from the five countries met together last November to coordinate their investigations into Mendes’s dealings over the two years when, they estimate, his turnover in fees received for negotiating transfers of numerous players between clubs totalled about 1.2 billion euros.

Among the dozens of sports figures managed by Mendes, 52, are Manchester United manager Jose Mourinho, Paris Saint-Germain’s Argentine player Angel di Maria, and Bayern Munich midfielder James Rodríguez. Mendes was summoned to appear last October before the magistrates investigating Ronaldo’s alleged tax fraud, and earlier in 2017 appeared before magistrates in Madrid in a closed-door hearing into the separate case of alleged tax evasion by Colombian footballer Radamel Falcao, accused of evading taxes on 5.6 million euros in image rights earnings when he played for Atletico Madrid in 2012 and 2013.

Mendes has strongly denied wrongdoing in both the affairs of Ronaldo and those of Falcao, who this year reached a financial settlement with the Spanish tax authorities after he admitted the fraud.

The documents obtained by the EIC show that a company called CRS Holding was created in Luxembourg on May 26th 2015, apparently primarily for the purpose of managing Ronaldo’s commercial partnership with the Portuguese hotel group Pestana for the opening of a series of so-called “lifestyle” hotels branded with his initials and football shirt number, Pestana CR7 https://www.pestanacr7.com/en . But Cristiano Ronaldo’s name did not figure on the company registration documents. Instead, the sole shareholder of the Luxembourg company is a Jersey-registered trust called CRS Holding Trust, whose unique beneficiary is Cristiano Ronaldo (see below).

Enlargement : Illustration 3

There is nothing illegal about owning a trust in Jersey. However, in the footballer’s 2015 tax statements to the Spanish authorities, while he did declare being the beneficiary of a bank account in the name of CRS Holding, in which there was then 197,000 euros, there was no mention of the existence of the CRS Holding Trust in Jersey.

Just how much wealth was managed by the Jersey entity is unknown, but what is clear is that between June 2017 and March 2018, the CRS Holding Trust transferred 16 million euros into its Luxembourg subsidiary CRS Holding.

Contacted on April 16th by Mediapart’s EIC partner Der Spiegel, neither Ronaldo nor his agent, Jorge Mendes, replied to the EIC’s questions, notably the value of the assets of the CRS Holding Trust and whether Ronaldo was required to declare these to the Spanish tax authorities. However, on Friday, April 20th, shortly after Mediapart and its EIC partners published their first reports on the issues raised here, a lawyer representing Ronaldo sent an email to two other EIC partners, the Spanish daily El Mundo and Portuguese weekly Expresso, in which he adjoined several documents. The lawyer said Ronaldo’s ownership of Luxembourg company CRS Holding had been declared to the Spanish tax authorities (which the EIC partners had made clear in their reports), and that the footballer complied with the requirements of the tax authorities.

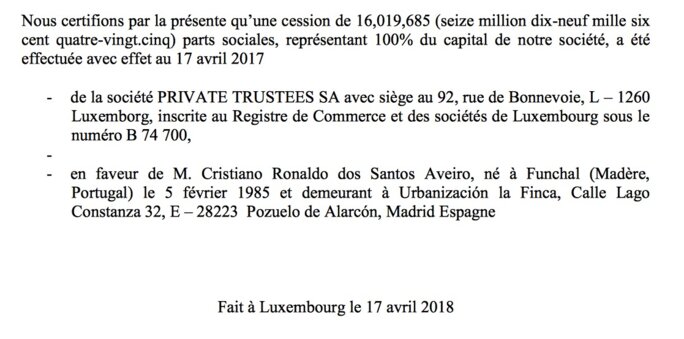

Meanwhile, the lawyer made no reference to the CRS Holding Trust in Jersey with regard to his tax statements. However, one of the documents he sent in his email to the EIC partners showed that Ronaldo had dissolved the trust in Jersey on April 17th, just 24 hours after EIC partner Der Spiegel had sent, last Monday, its questions about the entity. Another document showed that the same day that the Jersey trust was wound down, last Tuesday, Ronaldo was made the direct beneficiary of the Luxembourg company CRS Holding (see the relevant extract of the document immediately below).

Enlargement : Illustration 4

Ronaldo has previously insisted that he has always been clear and honest in his tax dealings. After the publication by the EIC partners in December 2016 of documents showing how Ronaldo had channelled just under 150 million euros earned from commercial deals into the Caribbean tax haven of the British Virgin Islands and also in Switzerland, he told French football magazine France Football: “It hurt me because we always try to do things well. When they talk about me, and the way they do it, I don't feel good. There are a lot of innocent people in prison, and I feel like that. You know you didn't do anything wrong, and they tell you that you did something reprehensible.”

The star has since hired the services of tax lawyers from a leading Spanish law firm owned by Spain’s current treasury minister Cristóbal Montoro.

Meanwhile, the EIC has learnt that tax officials from Britain, Cyprus, Ireland, the Netherlands, Portugal and Spain met in secret in a Lisbon hotel last November 21st and 22nd as part of their conjoint investigations into the financial affairs of Ronaldo’s agent Jorge Mendes, who is a tax resident in his native Portugal. The multi-national investigations, launched on the initiative of the Portuguese authorities, centre upon three of Mendes’s companies: Gestifute, which manages football players and other sports figures (such as with transfers between clubs and wage agreements), and MIM and Polaris, which manages sponsorships and image rights.

Enlargement : Illustration 5

In 2015 and 2016, when it is estimated that transfer deals managed by Jorge Mendes totalled 1.2 billion euros, the agent’s companies paid out 42.5 million euros in dividends. Up until 2012 Mendes was the direct owner of his management companies, but after that the ownership was placed behind Start BV, a company registered in the Netherlands where dividends are subject to comparatively minimal taxation.

The joint investigations launched last year are also focussed on determining the exact nature of relations between Mendes and a Cyprus-registered company called Browsefish, which operates as an investment fund which is owned by Russian businessman Dmitry Rybolovlev, president of French football League 1 club AS Monaco.

Documents obtained by the EIC from the platform Football Leaks indicate that before the current conjoint investigations into his tax affairs, Mendes hired a law firm at considerable expense to prepare his defence against accusations of tax fraud, as illustrated by the heading above invoices from the lawyers, seen by the EIC, explicitly titled “Tax fraud Jorge Mendes”.

-------------------------

If you have information of public interest you would like to pass on to Mediapart for investigation you can contact us at this email address: enquete@mediapart.fr. If you wish to send us documents for our scrutiny via our highly secure platform please go to https://www.frenchleaks.fr/ which is presented in both English and French.

-------------------------

- The French version of this article can be found here.

English version by Graham Tearse